The Auditor General’s report into 1MDB is written in professional and dispassionate language. However, no one could fail to miss the stark criticism and disapproval contained within those paragraphs of factual analysis.

Preceding over 330 pages of tight scrutiny of the evidence made available to him (which he points out was not nearly as much as he would have wished or expected) the AG provides the usual ‘Executive Summary’ for such reports, focusing on the key information and points to be made.

From this Executive Summary we today translate his analysis of the fate of the original US$1.83 billion investment into the PetroSaudi Joint Venture and the next follow up investment into the 1MDB subsidiary SRC International, using money primarily borrowed from the public pension fund KWAP.

His task was made considerably more difficult he says, owing to the fact that 1MDB failed to provide much of the normal documentation an auditor would expect to perform their task:

“JAN [Auditor’s Department] faced limitations while performing this audit in view of the fact that some original or important documents were either submitted late or were not provided by 1MDB for the purpose of verifying transactions or as evidence for the audit.….

The limitations resulted in a significant impact on the audit process in terms of verification of the actual financial position, operations and related transactions. Among important documents that were not submitted were the 1MDB Group’s Management Account for the year ending March 31, 2015 and bank statements from foreign lenders. [The audit team] was unable to access computers, notebooks and servers at 1MDB in order retrieve data and information for cross reference and analysis…”

Executive Summary

The AG sets off by laying out his task, required both by the Cabinet and the Public Accounts Committee, to examine the performance of 1MDB.

He notes the company was originally set up as a sovereign wealth fund, based on Terengganu’s oil reserves, but that the management under CEO Shahrol Halmi fell out with the shareholders in the Terengganu state government almost immediately, because Halmi went ahead with issuing a RM5 billion Islamic Medium Term loan (ITMN) through AmBank, without gaining the appropriate consent of Terengganu.

On July 31st, therefore, the fund was re-launched as 1MDB entirely under the purview of the Ministry of Finance. The AG notes [2.1.3.] that the Sultan and MB of Terangganu had complained of “malpractice” and “non-compliance” and had accused AmBank of “unauthorised issuance” of the bonds during its dispute with Halmi.

The AG also informs [2.1.4.] that the bond appeared to have been raised from its anonymous lenders at a very punishing rate – those lenders only paid RM87.92 for every RM100 in nominal value “to ensure the issuance of the IMTN was fully subscribed”, he said. He adds that “the coupon rate is 5.75% per annum with effective rate of returns to be 6.68% annually”. To raise this RM5 billion will cost a total of RM11,90 billion to pay back at these punishing rates the Auditor has noted:

The IMTN issued in 2009 will mature in 2039 with coupon payments amounting to RM287.50 per annum. 1MDB Group’s commitment for the IMTN from November 2015 until 2039 amounts to RM11.90 billion – RM5 billion principle and RM6.90 billion in interest.[6.6 – Executive Summary]

These expensive terms for the loan are known to have been a source of controversy at the time and 1MDB has throughout its existence followed a pattern of such apparently unnecessarily expensive borrowing, which has added considerably to its financial problems and has never been properly explained by the Finance Minister.

PetroSaudi Venture

After outlining such an unpromising start Auditor General, Ambrin Buang, proceeds to outline the first venture in 1MDB’s stated “goal of pioneering investment opportunities abroad”, which was the joint venture with PetroSaudi, signed 28th September 2009.

The AG sums up his disapproval in the following terms:

“The decision to invest in this JV company was made in a period of eight days, without a detailed evaluation process and before issues/conditions raised by the 1MDB Board of Directors were resolved. There were four different companies registered with the name PetroSaudi but the investment proposal paper tabled to the 1MDB Board of Directors did not state this fact.” [2.2.1.]

The Auditor continues with a withering dismissal of the “valuation” of the company provided by a pal of PetroSaudi Director Patrick Mahony, namely the CitiGroup Executive Ed Morse, who was paid US$100,000 for a few hours work:

“The assets valuation report prepared by Edward L Morse was presented on Sept 29, 2009, which is the same date that he was confirmed in his appointment to perform the job by the 1MDB CEO, and the report was received one day after the JV was signed…. The valuation was conducted on assets owned by PetroSaudi International Ltd although the JV agreement clearly states that the company which owned all rights and interests on the agreed assets for the JV project was PetroSaudi International Cayman.” [2.2.2.]

Wow! They valued the wrong company – how come?

The AG goes straight on to complain that this agreement “includes clauses that insufficiently provide for the interest of the company [1MDB]”. Among these disadvantageous provisions he names the US$700 million “loan”, which was tagged onto the subsidiary that PetroSaudi injected into the joint venture just a couple of days before the deal was signed, on the understanding that the joint venture would then pay it back!

“The payment of USD700 million to the other company was performed without the approval of the 1MDB Board of Directors” confirms the AG [2.2.3.]

Murabahah Notes

Just six months after all this song and dance the whole investment arrangement was altered, writes the AG (you can visualise his eyebrows raising).

1MDB jacked in the whole investment in return for US1.2 billion worth of “notes”, guaranteed by PetroSaudi itself. This was followed by further ‘Murababaha’ (Islam-friendly) borrowing of US$500 million and then US$330 million – a total of US$1.83 billion [2.2.4.].

All change again!

This arrangement lasted barely two years the AG continues, before 1MDB altered its investment again. This time it converted its borrowing back into shares directly in PetroSaudi, buying a 49% stake in its subsidiary PetroSaudi Oil Services Ltd (PSOSL):

“The swapping of Murabahah Notes for equity in PSOSL was performed without detailed study to determine (PSOSL’s) liability, ability to generate funds and its past financial performance”, notes the AG with a dry sigh [2.2.5.],

This was despite the fact that knowledge of PSOSL’s operations in Venezuelan waters was subjected to restrictions/sanctions by the US and that the company’s drilling contracts were expiring. Naturally, the plainly unwise investment was done in advance of any kind of Board approval:

“Moreover, the approval by the Board of Directors and 1MDB shareholders to swap the Murabahah Notes for equity in PSOSL was signed on June 20, 2012, but the 1MDB CEO had signed five documents regarding the deal on June 1, 2012. This shows that the 1MDB CEO took action even before seeking the board’s approval” [2.2.6.]

Ooops! change again!

It took only 45 days for 1MDB to change its mind about this investment, continues the AG. He details how the fund cashed out its PSOSL shares Sept 12 2012 in a deal with the little known fund managers Bridge Partners.

Bridge Partners were supposed to pay a handsome price of US$2.3 billion for these shares, according to the ‘sale purchase agreement’, which was advertised by 1MDB as a successful profit on its original US$1.83 billion investment into this series of PetroSaudi related enterprises.

But, in the end the expectation of much needed cash (1MDB’s other investments were causing major cash flow issues by this stage) was replaced by ‘notes’. An “Investment Management Agreement” made on the same day with Bridge Partners allowed for its ‘payment’ to 1MDB to be converted into an investment into its own Segregated Portfolio Company (SPC) in the Cayman Islands. This, says the AG, “was funded through promissory notes in lieu of cash”.

Given that the advertised material relating to this Cayman Island Fund warns investors that they could easily lose all of their investment, these “promissory notes” would appear to be a very poor bargain for the hard currency profit boasted of in 1MDB press releases and Ministry of Finance statements. The AG adds with a note of utter exasperation:

“This Investment was made through Bridge Global Absolute Return Fund SPC (Bridge Global SPC), which was a month-old company, without a fund managing license and without experience in managing large sum of funds” [2.2.8.].

The words criminally irresponsible come to mind, although they would not be uttered by any auditor in such a context, and indeed the chaps in charge of the fund’s ultimate controllers Avestra, were soon facing criminal charges over the management of this fund in Australia.

Credibility Crisis

By this stage of his synopsis the Auditor General records that 1MDB’s own Board had concluded that they had a massive PR problem on their hands, owing to such a lamentable investment history at the fund. The Board wanted the cash brought back to Malaysia says the AG, but the management (as usual) refused to play ball:

“[2.2.8.] The Board of Directors on May 20, 2013 agreed that the investment be redeemed in stages in order to improve public perception on the credibility of 1MDB’s investments. The Board of Directors had issued nine instructions between May 2013 and August 2014 to the management to prepare a plan, schedule and redemption of portfolio funds from the SPC either through stages or as a whole. However, no immediate action was taken by the 1MDB management.

Eventually, on 20th December 2014, Buang confirms the Board were told at a meeting that USD1.392 billion had been redeemed from this Cayman SPC. The remainder, they were informed (US$993 million) would be used to ‘terminate options with Aabar’. But, again, says the AG, the management did not do what they had agreed to with the money:

“In reality, all of those remaining funds from the SPC portfolio were used as collateral for Beutsche Bank for a loan amounting to USD975 million, for which an approval from the Board of Directors was not obtained. Apart from this, the USD1.392 billion which had been transferred to the account of Brazen Sky Ltd was forwarded to 1MDB Global Investment Limited (1MDB GIL). This act contravened the instructions of the Board of Directors who demanded that the SPC portfolio funds be brought back to Malaysia.” [2.2.9]

It really is as breath-taking stuff as you are likely to read from a crusty Auditor’s Report into a government owned company. Najib for one had plainly expected a bland whitewash, along the lines of 1MDB’s own purchased audits.

As we all know by now, the AG has also pointed out in related papers that no proof was ever produced by the rogue management of the company that any hard cash in reality ever returned from the Caymans. There were simply no bank accounts or documents produced by 1MDB to substantiate its various claims.

To the contrary, it is already known that most of the money (US$1.03 billion) “invested” in PetroSaudi disappeared on Day 1 into Jho Low’s outfit, Good Star Limited. and a further US$260 million went into the buy out of UBG, so how could US$2.3 billion have been realised. And don’t forget the interest payments!

SRC International

The Auditor General had the same experience of negligent behaviour when he examined the controversial SRC International, he said, a company that was rapidly pulled out of 1MDB and place under the Ministry of Finance, away from the scope of this enquiry:

For example:

“The SRCI board approved USD45.50 million for investment in the coal industry in Mongolia without providing a feasibility study on the matter ..” [3.3]

In conclusion, writes the exasperated AG [2.2.12] “for the period of four years since 1MDB was established… this investment instrument was changed four times.” He sums up the present situation:

“6.3 An analysis of the cash flow on the financial statements from year 2010 to 2014 have shown that 1MDB’s paid-up capital was only RM1 million. This small amount showed that the company was not (financially) stable because it required to borrow for its activities. Throughout financial year 2010 until 2014, 1MDB obtained 17 loans (not inclusive of inherited loans) at a nominal value of RM42.88 billion but received cash amounting to RM39.17 billion.However, (the company’s) activities which were funded by loans did not generate the necessary cash flow to repay the loans……

“1MDB needs to prepare large sums to fulfil its obligations – RM4.88 billion in 2016, RM14.74 in 2023 and RM5.14 billion in 2039. 1MDB also requires to have at least RM1.52 billion annually from Nov 2015 to May 2024 to repay its loans.”

For this outrageous situation the AG blames the management, whose controls were “less than satisfactory” and which operated “without due process”. “Several important investment decisions involving large sums were made .. without any discussion and proper detailed valuation. Several investments were decided on short notice and were high risk.” he says. Moreover:

“In several situations, the 1MDB management had presented incomplete or inaccurate information to the Board of Directors before an important decision was to be made. In fact, the management sometimes took action without approval from the Board”

In short the Auditor General’s report confirms, after a professional and objective examination, all the criticisms that have been made of 1MDB’s financial mayhem and worse.

The decision to make it an official secret can therefore only be described as a disgraceful cover-up to protect the criminal negligence and misappropriations of the parties concerned.

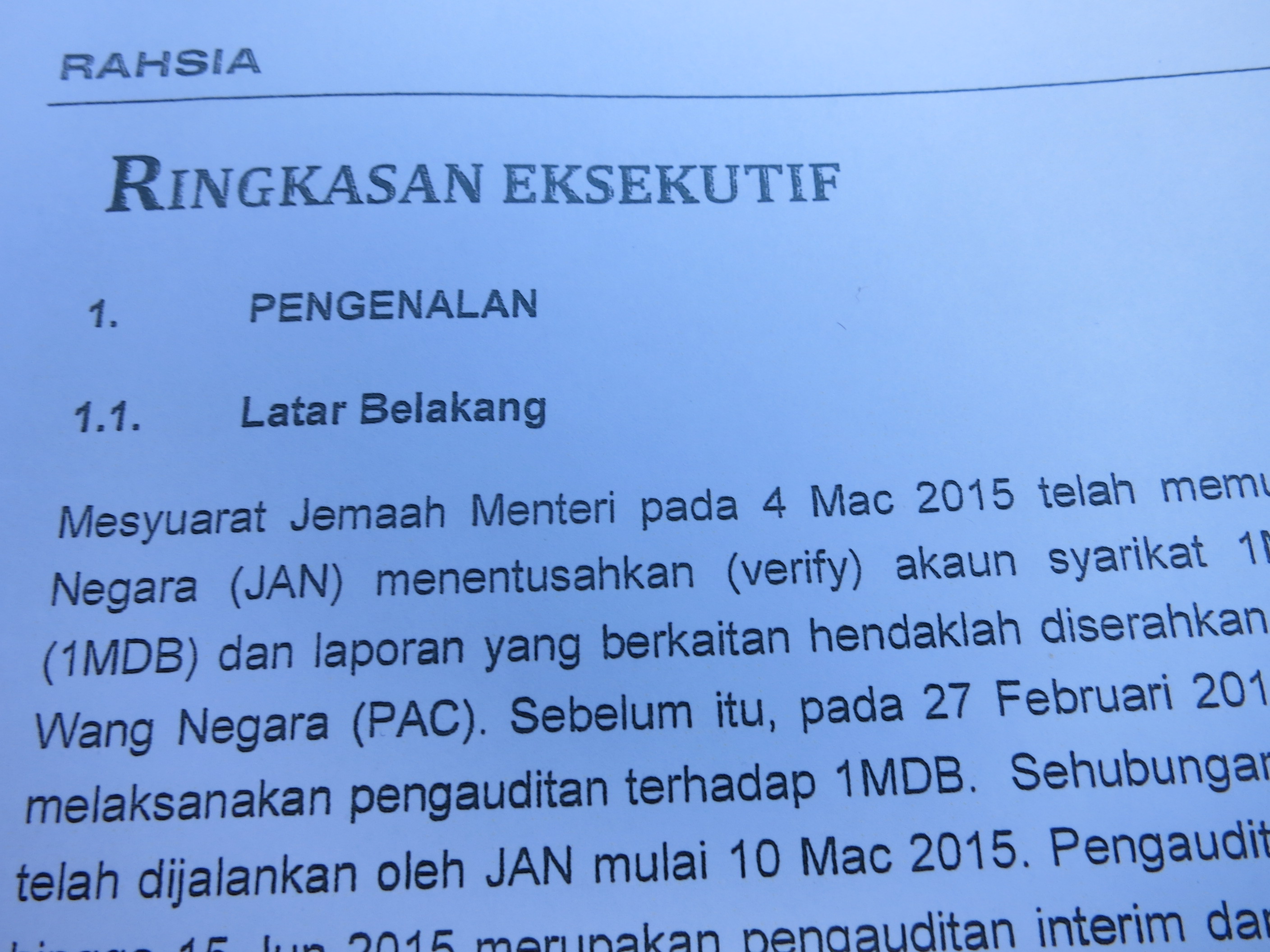

See excerpts from the EXECUTIVE SUMMARY